Buying a home is a huge step, and if you’re caught between loan options, you’re…

Spring is in the Air – But Will Lower Mortgage Rates Be Enough to Warm Up the Portland/Vancouver Market?

Spring is in the Air – But Will Lower Mortgage Rates Be Enough to Warm Up the Portland-Vancouver Market?

After weeks of rain and gray skies, the sun is finally making an appearance, and signs of spring are emerging. Daffodils are peeking through, and there’s a hopeful feeling that brighter days are ahead. But what about the housing market? Is it warming up, too?

Mortgage rates have started to come down, which should be great news for homebuyers. Lower rates typically mean lower monthly payments and improved affordability. But just like the unpredictable spring weather, the real estate market remains a mix of optimism and uncertainty.

So, will lower rates be enough to bring hesitant buyers back, or will concerns over inflation, job security, and rising costs keep them waiting? Let’s break it down.

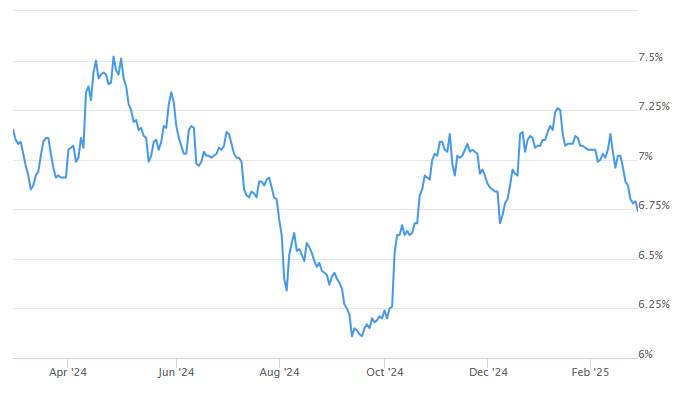

Mortgage Rates Are Falling – A Welcome Change

For the first time in months, buyers are getting a little relief:

🔹 30-year fixed mortgage rate: 6.74%, down from 6.85% last week—the lowest since December.

Even small rate drops can make a difference in monthly payments, but affordability remains a challenge.

Average Rate below as of 2/28/2025 (Source: Mortgage News Daily)

What’s Keeping Buyers on the Sidelines?

Lower mortgage rates usually help boost home sales, especially heading into the busy spring season. But this year, many buyers are still holding back. Here’s why:

💼 Economic Uncertainty – Job cuts, tariffs, and shifting policies are making some buyers nervous about making big financial commitments.

📈 Rising Inflation Expectations – Even as mortgage rates fall, the cost of living continues to rise, making affordability a concern.

📉 Market Volatility – Investors are moving toward safer options like bonds, signaling concerns about the overall economy.

These factors are helping push mortgage rates lower—but at the same time, they’re also making buyers more hesitant.

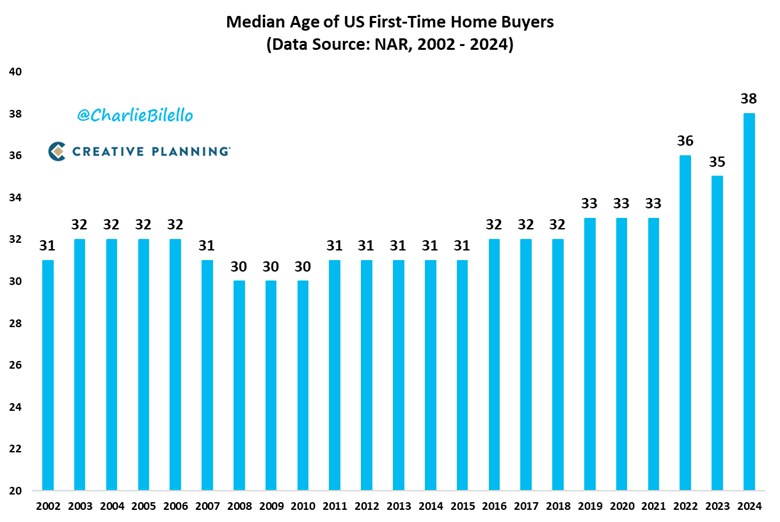

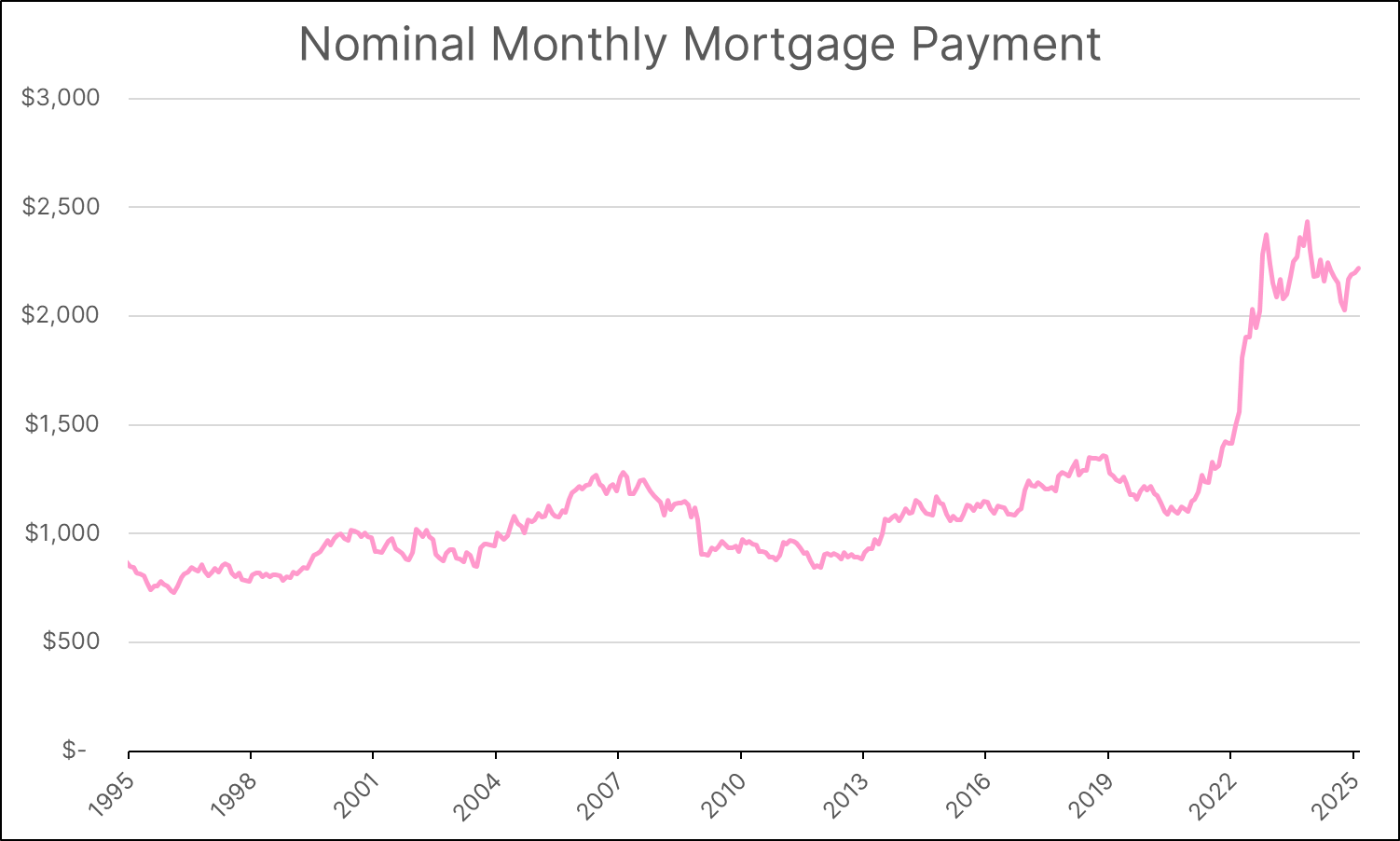

Affordability Remains a Major Hurdle

Even with lower rates, homeownership is still a financial stretch for many:

🏡 Only 17% of renters can afford a starter home, compared to 37% just a few years ago.

📆 First-time homebuyers are getting older, with the median age rising to 38 in 2024—the highest on record.

💰 The average monthly mortgage payment has jumped to $2,220, an 89% increase over the past five years.

With affordability stretched thin, buyers are taking on more debt than ever to make homeownership possible—especially those using FHA loans.

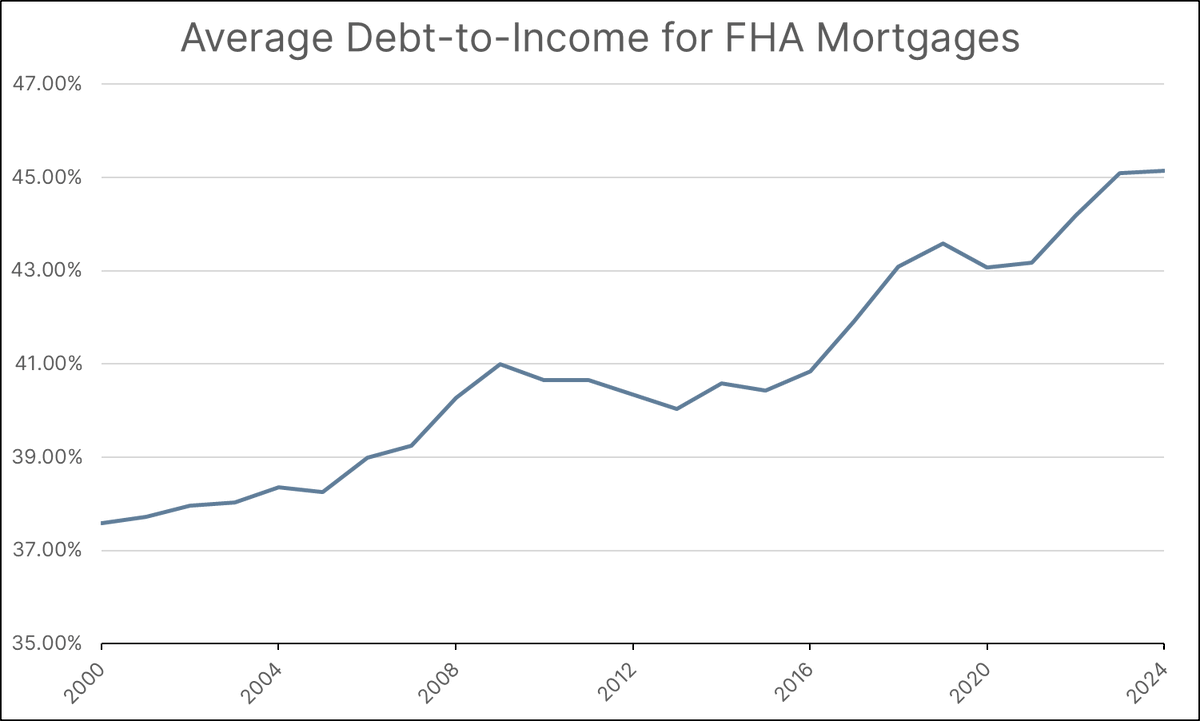

FHA Borrowers Are Carrying More Debt

FHA loans, which allow for lower down payments and more flexible credit requirements, have become a popular option for first-time buyers. But recent trends show that many FHA borrowers are stretching their budgets:

🔢 31% of FHA mortgages now have debt-to-income (DTI) ratios above 50%—a significant jump from just 6% in 2000.

📊 The average DTI for FHA borrowers has climbed to 45%, compared to 41% during the 2008 housing crisis.

📉 More than 64% of FHA mortgages now go to buyers with DTIs exceeding 43%, a reversal from past trends.

While these looser lending standards are helping more people qualify for home loans, they also come with increased financial risk.

What Does This Mean for Homebuyers?

The housing market is sending mixed signals, and buyers should be prepared to navigate a complex landscape. Here’s what to consider:

✔ If you’re waiting for rates to drop further – Rates are improving, but economic uncertainty means they could fluctuate. Locking in a lower rate now might be a smart move, especially if home prices rise in the future.

✔ If you’re concerned about affordability – Exploring creative financing solutions, such as rate buydowns or adjustable-rate mortgages, could help lower your monthly payments.

✔ If you’re using an FHA loan – Be mindful of your debt-to-income ratio. Taking on too much debt could make future financial challenges harder to manage.

✔ If you’re unsure about the market – Talking to a mortgage professional, such as me, can help you weigh the pros and cons based on your specific situation.

The Bottom Line

Like the break in the weather, the housing market is showing signs of change. Mortgage rates are dropping, but economic uncertainty still looms. Buyers are stuck between opportunity and hesitation.

If you’re thinking about buying a home, now is the time to get informed. Understanding your options, weighing the risks, and having a solid financial plan will help you make the right move—whether that’s jumping in now or waiting for more stability.

What do you think—will lower rates be enough to bring buyers back, or will uncertainty keep them waiting? Drop your thoughts in the comments!

About the Author

Matt Jolivette

Mortgage Broker at Associated Mortgage Brokers · NMLS #90661

Matt Jolivette is one of two owners of Associated Mortgage Brokers and brings his clients 25 years of experience as a mortgage broker. Matt received his Bachelor of Science degree in Finance from Portland State University, studying and attending classes nights while working full time at Associated Mortgage Brokers, graduating in 2005.

Specializes in: Conventional, FHA, VA

Licensed in: ID, OR, WA

Related Posts